The Complete Guide to Home Loan Balance Transfer in India (2026)

The ultimate 2026 guide to home loan balance transfers in India. Learn the exact math to calculate real savings, compare lenders, and know when to switch.

Table of Contents

The RBI cut the repo rate by 125 basis points (1.25%) across 2025 — from 6.50% to 5.25%. As of April 2026, the Monetary Policy Committee (MPC) has held at 5.25% with a neutral stance. According to the central bank's own data, banks have passed through roughly 89 bps on fresh loans and 87 bps on existing loans. Do the subtraction. Almost 36 bps of cuts the RBI announced never reached your EMI.

Multiply that across the ₹430-billion-dollar Indian housing loan book, and you're looking at one of the largest, quietest wealth transfers in the country — from middle-class borrowers to the spread on every bank's net interest margin. If you have a ₹50 lakh home loan with twenty years remaining, those 36 missing basis points are worth roughly ₹1.4 lakh of interest you will pay, that the policy rate said you shouldn't have to.

This is the unglamorous truth of Indian home loans. The rate cut is announced on television. The transmission happens in the small print, on a quarterly reset cycle nobody told you about, in a city where the borrower has neither the time nor the leverage to chase it.

A balance transfer is the borrower's most powerful response. It is also the most poorly explained product in Indian retail finance — explained mostly by sites whose business model depends on you transferring to a specific lender.

This guide is the explanation you should have been given the day you signed your home loan agreement.

What a balance transfer actually is, stripped of marketing language

A home loan balance transfer is a refinance. Lender B pays off your outstanding principal at Lender A and creates a new loan in your name at, presumably, a lower interest rate. Your property's title is re-mortgaged to Lender B. You start paying Lender B's EMI from the next cycle.

That is the whole product. Everything else — "save lakhs," "lower EMI," "top-up benefits" — is marketing wrapped around this single mechanical fact: one lender writes a cheque to another, in exchange for the right to charge you interest going forward.

The reason it exists, and the reason it works, is that home loan markets are sticky. Most borrowers don't track their interest rate after Year 1. Most don't know if they are on EBLR or MCLR. Most won't move banks without a forcing function. So lenders price legacy borrowers worse than fresh borrowers — what bankers euphemistically call "back-book stickiness." Refinancing closes that gap. In a competitive market with an active rate-cut cycle, refinancing is not optional. It is hygiene.

The "Rs X lakh saved" math that gets everyone in trouble

Walk into any comparison site, type your numbers into their balance-transfer calculator, and you will see something like this: "Switch from 9.25% to 8.25% on your ₹50 lakh loan and save ₹6.4 lakh!"

That headline number is almost always misleading. Here's why.

To make the savings look enormous, the calculator quietly assumes one of two things: that your tenure remains exactly the same (and you save on lower interest), or — far more commonly in actual lender practice — that you reset the tenure back to 20 or even 25 years on the new loan, while keeping the EMI roughly constant. The second is the "EMI reduction" path the comparison sites optimise for, because a smaller EMI looks like a victory. It is not.

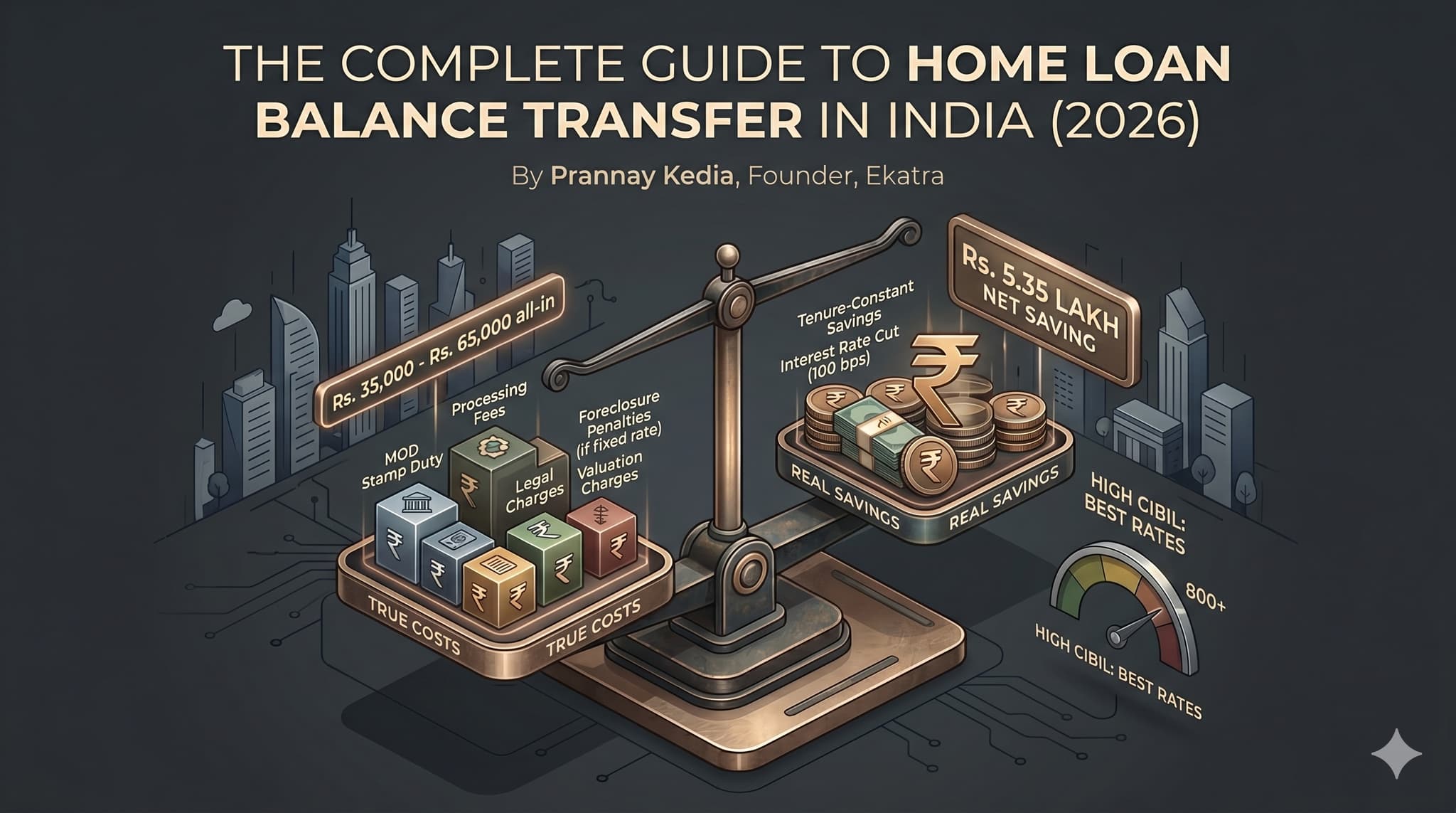

Take a real number. You took a ₹50 lakh loan at 9.25% for 20 years. EMI: ₹45,793. After five years, your outstanding principal is roughly ₹44.1 lakh. You have 15 years left.

Path A: You refinance the ₹44.1 lakh at 8.25% for the remaining 15 years. EMI drops from ₹45,793 to ₹42,816. Total interest from here: ₹32.97 lakh. Versus continuing at 9.25%: ₹38.32 lakh. Real saving: ₹5.35 lakh, before any switching cost.

Path B: You refinance ₹44.1 lakh at 8.25% but your new bank — generously — gives you a fresh 20-year tenure to "reduce your EMI." New EMI: ₹37,604. Looks great. Total interest from here: ₹46.13 lakh. Versus the old loan's ₹38.32 lakh. You have just paid ₹7.8 lakh more in interest, while believing you saved.

This is the tenure-reset trap. The savings calculators on most comparison sites compute Path B by default, but headline it as a saving figure derived from EMI reduction × old tenure. It is mathematical sleight of hand. The right benchmark is always: total interest paid, holding tenure constant, net of all switching costs.

Refinancing without holding tenure constant is not refinancing. It is a polite second mortgage.

The true cost of switching, including everything BankBazaar's calculator quietly omits

Comparison-site calculators present two numbers: rate differential, and "savings." A real switching decision involves at least seven costs.

- Processing fee. The new lender charges 0.25% to 0.50% of the loan amount, capped variously. SBI: 0.35%, capped at ₹10,000 + GST. ICICI: 0.50%. HDFC: 0.50% for salaried (min ₹3,000), up to 1.50% for self-employed non-professionals (min ₹4,500). Axis: typically 0.50%, often waived during festive periods. On a ₹50 lakh refinance, this is anywhere from ₹3,000 to ₹35,000 + GST. Festive waivers happen, but assume the fee unless you have it in writing.

- Stamp duty on the new Memorandum of Deposit of Title Deeds (MOD/MODT). When you refinance, the mortgage charge moves from Lender A to Lender B. In Maharashtra, under Article 6 of the Bombay Stamp Act, this attracts stamp duty of 0.3% of the loan amount. On ₹50 lakh, that's ₹15,000. In Karnataka, roughly 0.25%. In Delhi, the equivalent registration charge structures vary. This is not a fee anyone reimburses. It is a real, sunk transfer cost — and it is the single biggest line item the comparison sites tend to omit. Mumbai borrowers refinancing a ₹1 crore loan are looking at ₹30,000 of MOD stamp duty alone.

- Legal and valuation charges. Some lenders bundle this into the processing fee; others pass it through. Budget ₹3,000–₹8,000.

- Documentation and operational charges. CERSAI, franking, notarisation, courier of original property documents from old lender to new lender. ₹1,500–₹4,000.

- Insurance bundling pressure. This is the quiet one. Many lenders, particularly private banks and HFCs, will offer a sharper interest rate if you "agree" to bundle a credit-life insurance policy financed by the same lender. The policy is profitable for the bank — it earns a commission while you pay premium. The headline rate looks lower, but the all-in cost rises by ₹40,000–₹1,00,000 over the loan tenure on a ₹50 lakh loan. Always ask for the rate without the insurance. Always.

- Foreclosure charges on the old loan. Here is genuinely good news. The RBI's Pre-payment Charges on Loans Directions, 2025 (effective on all loans sanctioned or renewed from January 1, 2026) prohibit foreclosure or pre-payment charges on floating-rate loans to individuals for non-business purposes — including housing loans — irrespective of the source of funds, without any minimum lock-in period. If your existing loan is floating rate (and the vast majority of EBLR-linked loans are), your old lender cannot charge you to leave. This was already true under the 2012 and 2014 circulars; the 2025 Directions tightened and unified the regime. If your loan is fixed-rate, foreclosure penalties of 2–4% of the outstanding can still apply.

- Time cost. Twenty to thirty days. Multiple branch visits or video KYC sessions. Re-execution of property documents. For most middle-class salaried borrowers, the opportunity cost of the time and the friction of the process is the single most underrated reason refinancing doesn't happen even when the math is obvious.

Add it up. For a ₹50 lakh refinance in Maharashtra, all-in switching cost typically lands in the ₹35,000 to ₹65,000 range, before any insurance bundling. Not the ₹0 the marketing implies. Not the ₹2,000 the front-end shows. A real number, paid in real cash.

The break-even framework (when refinancing actually pays)

Once you have an honest cost number, the question becomes - how long before the refinance pays for itself?

The arithmetic is simpler than the comparison sites pretend.

Three worked examples, on remaining principal of ₹44 lakh, 15 years remaining, all-in switching cost of ₹50,000:

| Old rate → New rate | Old EMI | New EMI | Monthly saving | Break-even |

| 9.25% → 9.00% (25 bps) | ₹45,279 | ₹44,612 | ₹667 | 75 months (6.3 yrs) |

| 9.25% → 8.75% (50 bps) | ₹45,279 | ₹43,953 | ₹1,326 | 38 months (3.2 yrs) |

| 9.25% → 8.25% (100 bps) | ₹45,279 | ₹42,653 | ₹2,626 | 19 months (1.6 yrs) |

The widely repeated thumb-rule — "refinance if you can save at least 50 basis points" — is roughly right for borrowers with 10+ years remaining, where a 50 bps differential typically clears switching costs in three to four years. Below 25 bps, refinancing rarely pays unless your switching cost is genuinely zero (some PSU banks during festive offers come close). Above 75 bps, it almost always does, and the fact that you haven't refinanced is itself the evidence that the home loan market is broken.

A second factor: how much tenure remains. If you have less than five years left on your loan, the principal is small, the interest component of each EMI is small, and even a 100 bps cut translates to negligible absolute savings. The general rule — refinancing is a Year 1 to Year 12 decision on a 20-year loan; after that, the math gets thin.

A third factor that comparison sites rarely mention: outstanding principal. The same rate cut on a ₹30 lakh outstanding versus a ₹1 crore outstanding produces wildly different absolute savings. On a ₹30 lakh loan with 15 years left, a 50 bps saving works out to about ₹903 a month — clearing a ₹40,000 switching cost in roughly 44 months. On ₹1 crore, the same 50 bps saves about ₹3,012 a month — clearing the same cost in 14 months. Bigger loans refinance faster. This is intuitive once stated, ignored everywhere.

Use Ekatra's break-even calculator to run the numbers for your exact loan. It holds tenure constant, includes Maharashtra/state-specific MOD stamp duty, factors in actual processing fees by lender, and tells you the break-even in months — not the headline lakh-rupee figure.

CIBIL is the most undersold lever in Indian home loan pricing

Lenders quote rate cards. The cards are anchored to CIBIL bands. The bands are wider than most borrowers realise.

Industry pricing data through 2025–26 shows roughly the following spread between CIBIL bands for the same lender and loan size:

- CIBIL 800+ : best rate (often the headline "starting from" number)

- CIBIL 750–799 : +10 to +20 bps

- CIBIL 700–749 : +30 to +60 bps

- CIBIL 650–699 : +75 to +125 bps, conditional approval

- CIBIL <650 : rejection or significantly higher pricing

On a ₹50 lakh, 20-year loan, the difference between an 800 CIBIL and a 700 CIBIL borrower at the same lender is typically 50–75 bps of rate. That's roughly ₹1,800–₹2,700 a month on EMI. Over 20 years, ₹4–6 lakh in interest. The cost of a single delayed credit card payment — repeated over a few months — is essentially this much, baked into your home loan.

If your CIBIL has improved since you took your original loan — most middle-class borrowers' scores rise meaningfully in the 3–5 years after taking a home loan as their credit history deepens — that improvement is worth real money. The lender does not automatically reprice you. You have to either negotiate or refinance to capture it.

Before any balance transfer, do the boring work for 30 to 60 days: pull your CIBIL report, dispute errors (a surprising fraction of reports contain them), pay down credit card utilisation to under 30%, avoid hard enquiries, and don't close old credit accounts that lengthen your credit history. A 30-point CIBIL improvement before you apply can move you across a band and capture an additional 25 bps of rate. That is not a trick. That is just what risk-based pricing means in practice.

Negotiate first (Switch only if they refuse)

Almost every guide skips this step, because it generates no commission for anyone. So I'll spend a paragraph on it.

Before you apply for a balance transfer, write to your existing lender. Cite the specific competitive rate you have been pre-approved for elsewhere — even better, attach a sanction letter. Ask for an interest rate reduction. Most banks have an internal "rate switch" or "conversion" facility, where they will reduce your rate to closer to their current card rate in exchange for a small conversion fee (typically 0.25%–0.50% of outstanding, capped). For an existing borrower with a clean track record, this is operationally far cheaper for the bank than acquiring a new customer; many will offer 25–50 bps off without much fight, because losing a performing home-loan customer is genuinely painful for them.

If your current rate is 9.25% and the market is at 8.25%, ask for 8.50%. You may get it. You will pay ₹15,000 in conversion fees instead of ₹50,000 in switching costs, and you will not spend a month chasing documents. If they refuse — and some will, particularly NBFCs and HFCs that have priced you aggressively for back-book retention — then refinance. The act of asking costs nothing. The cost of not asking is everything you might have saved.

Where the lenders actually stand in 2026

Card rates published in early 2026, for borrowers with a strong credit profile (CIBIL 750+, salaried, ₹30L–₹1Cr loan):

Public sector banks anchor the lower end of the market and have transmitted the 2025 rate cuts most aggressively because their loans are predominantly EBLR-linked.

- SBI: 7.50% onwards. Processing fee 0.35%, capped at ₹10,000 + GST. Frequently offers concessional waivers and 5-bps women's discounts.

- Bank of Baroda: 7.45% onwards. Processing fee up to 0.50%. Reduced rate of around 7.20% available for top-tier profiles.

- PNB: 8.00% onwards on RLLR-linked products.

- Union Bank, Canara Bank, Bank of India: clustered between 7.35%–7.85%.

Private banks typically price 25–75 bps higher but compete on processing speed, digital experience, and pre-approved offers for existing relationship customers.

- ICICI Bank: 7.45% onwards, repo-linked.

- HDFC Bank: 7.90% onwards (some product categories range 8.45%–9.30%, particularly for self-employed non-professionals).

- Axis Bank: 8.00%–8.35% onwards, with rates extending higher based on loan size and profile.

- Kotak Mahindra Bank: 7.70% onwards.

Housing Finance Companies (HFCs) are a mixed bag. The strongest — LIC Housing Finance, Bajaj Housing Finance, Tata Capital — offer competitive rates around 7.15%–7.50%, often willing to underwrite borderline profiles that banks reject. The weaker HFCs (smaller, regional, or affordable-housing-focused) charge 9.5%–11%+ and are where the 2024–25 rise in housing-finance NPAs has concentrated. PSBs vs private banks vs HFCs is less a quality distinction than a profile-fit one. A PSU bank suits a salaried, well-documented borrower with patience for slower processing. A private bank suits a borrower who values speed and an existing banking relationship. An HFC suits a self-employed borrower whose income narrative is harder to fit into a bank's templated underwriting.

A note on the rate cards: these are starting rates, advertised to look attractive. The rate you actually receive is your CIBIL band's rate, plus any spreads for loan size, employer category, and whether you're salaried vs self-employed. Always demand the sanction letter with the exact rate before you commit.

The mechanics of switching, end to end

The process, executed correctly, takes 15–30 days. Executed badly — which is the modal experience — it can stretch to 60.

You begin with the new lender. Apply, submit documents, get a sanction letter with the exact rate and tenure. Once you have the sanction in hand, write to your existing lender requesting a foreclosure quote (the precise outstanding amount as on a future date) and a "List of Documents" — the property papers they hold. The new lender pays the foreclosure amount directly to the old lender. The old lender releases your property documents — usually after the cheque clears, sometimes after a few days of "processing" that exists primarily to slow you down. The new lender lodges a fresh MOD at the sub-registrar's office, paying stamp duty. You start paying the new EMI.

The documents you'll need (have these ready before you apply, or you will lose two weeks): KYC (Aadhaar, PAN, address proof), last 3 months' salary slips, last 6 months' bank statements showing EMI debits, last 2 years' Form 16 or ITR, the original loan sanction letter from the existing lender, the most recent loan statement showing outstanding principal, the foreclosure quote, the List of Documents from the existing lender, and copies of all property papers.

The most common rejection reasons are mundane and avoidable: CIBIL below the lender's threshold, FOIR over 50–55% (particularly common for borrowers who have taken car loans or credit card EMIs in the interim), discrepancies in property valuation, encumbrances on the title, or a property that falls outside the new lender's "approved projects" list. PSU banks reject more often on property/legal grounds; private banks reject more often on profile/income grounds.

When NOT to do a balance transfer

A balance transfer is sometimes the right answer. It is sometimes a costly distraction. Honestly, the second is more common than people admit.

Don't refinance if:

- You have less than 5 years remaining and the rate differential is under 75 bps. The math doesn't work.

- Your current lender has already agreed to reduce your rate to within 25 bps of the best available alternative. Take it.

- Your CIBIL has dropped since the original loan. You will get a worse rate, not a better one.

- You are mid-construction on an under-construction property. Refinancing during the disbursement phase is operationally painful and most lenders quietly avoid it.

- The reason you want to refinance is to get a top-up loan for a non-housing purpose (renovation funded with home-loan-rate capital is fine; using a home loan top-up to buy a car or fund consumption is the classic 22% personal-loan-priced-as-8.5%-home-loan trick that leaves you mortgaging your house for unrelated debt).

The marketing pretends balance transfer is universally beneficial. It isn't. About 30–40% of the borrowers who run their numbers honestly through Ekatra's calculator find that their best move is to negotiate with the existing lender, not to switch.

The incumbents' conflict of interest, said plainly

It is impossible to write this guide honestly without naming the structural problem in Indian online home-loan content.

BankBazaar's reported revenue is around $90 million annually, generated almost entirely through commissions paid by partner banks for successful loan applications. Paisabazaar, owned by PB Fintech, takes commissions of approximately 1–3% of the disbursed loan amount from its lender partners. Their public-facing model is "neutral comparison." Their actual model is lead generation: every comparison page, every "best home loan" article, every balance transfer calculator is an instrument for funnelling traffic to the lenders that pay the highest commissions — which, in housing finance, tend to be the higher-rate HFCs and private banks, not the cheapest PSU options.

This shapes their content in ways that are easy to miss until you look for them. The "savings" headlines optimise for the largest-looking number, which is the tenure-reset version. The fee disclosures are partial. The MOD stamp duty is rarely mentioned. The processing fee is shown but the insurance bundling — the largest hidden cost in many private-bank refinances — is treated as an upsell rather than a cost. The ranked tables of "best lenders" tend to feature the bank running a campaign that month, not the bank objectively offering the best rate to your CIBIL band.

I am not suggesting bad faith. I am suggesting that the business model determines what gets emphasised and what gets buried, and that a borrower who reads only the comparison sites will systematically over-estimate the savings and under-estimate the cost. The fact that the largest "comparison" platforms in India are owned by lead-gen businesses, and that no large independent borrower-advocacy player exists in the home loan refinance space, is not an accident. It is the market.

Ekatra exists because we believe the Indian middle-class home loan borrower deserves an actor whose only revenue is from helping them save money — not from sending them to a particular lender. Whether you use us or not, the discipline is the same: assume the comparison-site number is too good to be true, do the tenure-constant math yourself, include all seven switching costs, and ask the existing lender first.

The adjacent decisions that change the picture

A balance transfer is rarely an isolated decision. It sits inside a larger set of choices about the home loan itself.

- Prepayment vs SIP. This is the most-asked, least-resolved question in middle-class personal finance. The math is straightforward, the answer is not. If your home loan is at 8.5% (effective rate after old-regime tax benefits roughly 6%–7% for a 30%-bracket borrower), and Indian equity has historically delivered ~12% CAGR over 15+ year periods, the SIP wins on expected value. ₹15,000 a month into an equity SIP at 12% over 15 years compounds to roughly ₹75 lakh. The same ₹15,000 prepaid monthly on a ₹50 lakh, 20-year loan at 9% saves around ₹22–27 lakh in interest and closes the loan ~7 years early. The expected-value gap favours the SIP. The risk-adjusted gap is closer, because prepayment savings are guaranteed and SIP returns are not. The honest answer for most borrowers: do both. Prepay aggressively to reduce psychological debt burden and capture the guaranteed return; run a parallel SIP to capture the equity premium. Skip the all-or-nothing framing.

- Top-up loans. Once you've refinanced and built equity, lenders will offer you top-up loans secured against your home, often at home-loan rates plus 25–50 bps. Used for a genuine home upgrade or in lieu of a far more expensive personal loan, this is sensible. Used to fund a car, a wedding, or consumption, it converts your house into collateral for short-term spending. Lenders push this product hard because it has high attach rates and low operational cost; the discipline is the same as with any debt — borrow at home-loan rates only for assets that justify a 20-year financing horizon.

- Joint loans and co-applicants. A joint home loan with a working spouse can effectively double the Section 24(b) interest deduction (₹2L + ₹2L) and the Section 80C principal deduction (₹1.5L + ₹1.5L), provided both are co-owners and both repay from their own incomes. For dual-income middle-class households in the old tax regime, this is one of the highest-impact tax structures in Indian personal finance. For balance transfers specifically, joint loans complicate the paperwork (both applicants must sign, both CIBIL scores are pulled) but rarely affect the refinance decision itself.

- Tax implications under the new regime. The single most important shift in the home-loan tax landscape is that the new tax regime — which most salaried borrowers are now defaulted into — does not allow Section 24(b) interest deduction on self-occupied property, nor Section 80C principal deduction. Section 80EEA has lapsed for new loans (it covered loans sanctioned April 2019 to March 2022). For a ₹50 lakh loan in early years, where annual interest may be ₹4 lakh+, the old regime's combined ₹3.5 lakh deduction can be worth roughly ₹1 lakh of actual tax saving at the 30% slab. If you have a sizeable home loan and have moved to the new regime by default, run the comparison; for many borrowers the old regime remains materially better. Section 24(b) is still available in both regimes for let-out property, where the entire interest paid is deductible against rental income (with the loss-set-off cap at ₹2 lakh). Stamp duty paid at purchase qualifies for Section 80C in the year of payment under the old regime.

Eligibility, briefly — because it determines what's possible

The standard FOIR (Fixed Obligation to Income Ratio) framework lenders use: total monthly debt obligations including the new home loan EMI cannot exceed 40%–55% of net monthly income.

For a salaried borrower on ₹50,000 net monthly income with no existing EMIs, at 8.5% interest and 20-year tenure, this translates to a sustainable home loan in the ₹19–24 lakh range — under most banks' eligibility math. On ₹75,000 net income, that rises to ₹35–45 lakh. On ₹1 lakh net, ₹50–60 lakh. These are FOIR-derived ceilings, not LTV ceilings; the latter is determined separately by the property's market value (typically capped at 75%–90% of value depending on loan size, per RBI master directions on housing finance).

A second-order point that matters for refinancing: your eligibility at the new lender is recalculated from scratch. If you have taken a car loan or accumulated credit card EMIs since your original sanction, your FOIR may have deteriorated even as your CIBIL improved. The new lender may sanction a smaller principal than your current outstanding, which is the most painful refinance failure mode — getting halfway through the process and discovering the new bank can only refinance ₹40 lakh of your ₹44 lakh outstanding. Always pre-check FOIR before you begin.

A note on whether to buy at all in 2026

A balance transfer optimises a decision you have already made. But the larger decision — whether to take a home loan in the first place — has shifted under your feet, and any comprehensive guide owes you the parenthetical.

In Mumbai's prime localities, a 2BHK costs ₹1.5–3 crore, generating rental income of ₹50,000–₹90,000 a month. That is a gross rental yield of roughly 2–3%. Bangalore, Pune, Delhi NCR look similar. Set against home loan rates of 8%–9%, the cost of capital exceeds the rental yield by a factor of three to four. The price-to-rent ratio in most metros now exceeds 30, which is the textbook "renting plus investing the difference outperforms buying" zone. The math has been this way for several years; what changed in 2026 is that with equity SIPs available at 12% CAGR expectations and home loan rates at 8%–9%, the opportunity cost of a metro home purchase is mathematically large.

This does not mean nobody should buy a home. It means: buy because you have decided you want to live in this house for 10+ years, not because you have been told property "always goes up" or that EMI is "forced saving." If your stay horizon is under 7 years, the transaction costs alone (5–10% of property value in stamp duty, registration, brokerage, GST on under-construction units) typically wipe out any appreciation. Tier-2 cities — Pune, Ahmedabad, Jaipur, Indore, Coimbatore — with price-to-rent ratios under 20 and 8–10% appreciation are a genuinely different market and the math favours buying earlier. Tier-1 metros are not.

If you already own and are mid-loan, this section changes nothing for you — you are not selling, you are optimising. Refinance hard.

What honest optimisation looks like

The reason this guide runs long is that the home loan refinance decision sits at an unhappy intersection: a product where the math is genuinely complicated, the fees are genuinely opaque, the marketing is genuinely misleading, and the stakes — five to ten lakhs of real after-tax money over the life of an average middle-class loan — are genuinely large.

A thoughtful approach has six steps and takes about a week of attention.

One, pull your loan statement and confirm the benchmark (EBLR vs MCLR), the spread, the reset frequency, and the exact outstanding principal. You'd be surprised how many borrowers don't know what their loan is linked to. Two, pull your CIBIL report, dispute any errors, and assess whether you've moved up a band since the original sanction. Three, write to your existing lender with a rate-reduction request, ideally backed by a competitor's pre-approval. Four, if rejection or insufficient reduction, run honest break-even math — tenure constant, all switching costs included — across two or three serious refinance candidates. Five, before signing anything, demand the sanction letter shows the exact rate, the processing fee, and explicit confirmation of no insurance bundling. Six, after refinance, set up a quarterly check on whether your reset has happened on schedule, and plan a small annual prepayment from bonus or surplus income to compress the tenure naturally.

This is not glamorous. It is mostly paperwork, arithmetic, and the discipline to ask uncomfortable questions of large institutions. But the people who do it save several lakh rupees over the life of their loan, and the people who don't, fund — quietly, every month — the spread between what the RBI announced and what their bank passed through.

We built Ekatra because we thought a generation of Indians who track their stock portfolios obsessively and renegotiate their broadband plans every year deserve a tool that handles their largest single financial liability with the same rigour. The platform is free. We don't take commissions from lenders. We are not a comparison site dressed up as advice. The break-even calculator holds tenure constant. The rate comparison shows you the all-in cost, including MOD stamp duty for your state. The execution layer handles the paperwork.

Whether you use us or not, the principle is the one I'd want my own family to follow: don't trust the headline saving number, do the boring math yourself, ask the existing lender first, and remember that the home loan you signed five years ago was priced for the borrower you were then — not the borrower you have become. The most quietly expensive thing in Indian middle-class finance is the rate you are paying because you haven't yet looked.

Look.

Ekatra is a free, AI-native home loan refinancing platform built for India's middle-class borrowers. We don't take lender commissions. We exist to execute the refinance decision properly — break-even math, lender comparison, paperwork, all of it. Visit joinekatra.com to run your numbers.